Why Being Single in the UK Can Break the Bank

- colinslaby

- Feb 16

- 7 min read

Single people typically face significantly higher living costs than those sharing expenses. On average, they spend around £8,000 more per year on essential items. A single earner on £60,000 pays over £4,800 more in tax and National Insurance than a couple earning £30,000 each.

In London, someone on the median UK wage may spend up to 80% of their disposable income on living alone. Among the UK’s 30 largest cities, London and Edinburgh are the most expensive for single residents, while Middlesbrough is the most affordable.

A comfortable retirement is also costlier for single people, who require a pension pot roughly £300,000 larger than each member of a couple.

Although single life is often portrayed as carefree and independent, rising living costs and structural tax disadvantages mean that living alone in the UK has become increasingly expensive. This analysis uses the latest official data to quantify the additional financial burden faced by single individuals—from housing and everyday bills to taxation and retirement planning.

How many people live alone in the UK?

Being single does not necessarily mean living alone; many single adults continue to live with parents, housemates, or in shared accommodation due to affordability. However, having an independent home remains the preferred goal for most people—and the point at which financial pressures become most apparent.

One-person households are more common in the UK than many assume. According to the latest ONS data, around 30% of the UK’s 28.6 million homes—equivalent to 8.4 million households—are occupied by a single individual, an increase of 11% since 2014.

The majority of people living alone are over 65, reflecting longer life expectancy and the higher likelihood of being single later in life.

Across other age groups, the share of people living alone has remained largely stable over the past decade, with only a 1% increase among those aged 25 to 44.

Going it alone but still at home

For many younger adults, being single no longer means moving into a one‑bedroom flat; instead, it often means remaining in the family home due to high housing costs. The number of young adults living with their parents has increased by 10% since 2014 and by more than one‑third since the mid‑2000s.

The largest rises among 25‑ to 34‑year‑olds are in areas like London, where house prices have risen the most. Although living with parents can come with challenges, it can also be financially advantageous: 14% of young adults in this situation increase their net wealth by more than £10,000 over a two‑year period. (higher with adequate financial planning)

Where solo-living costs the most

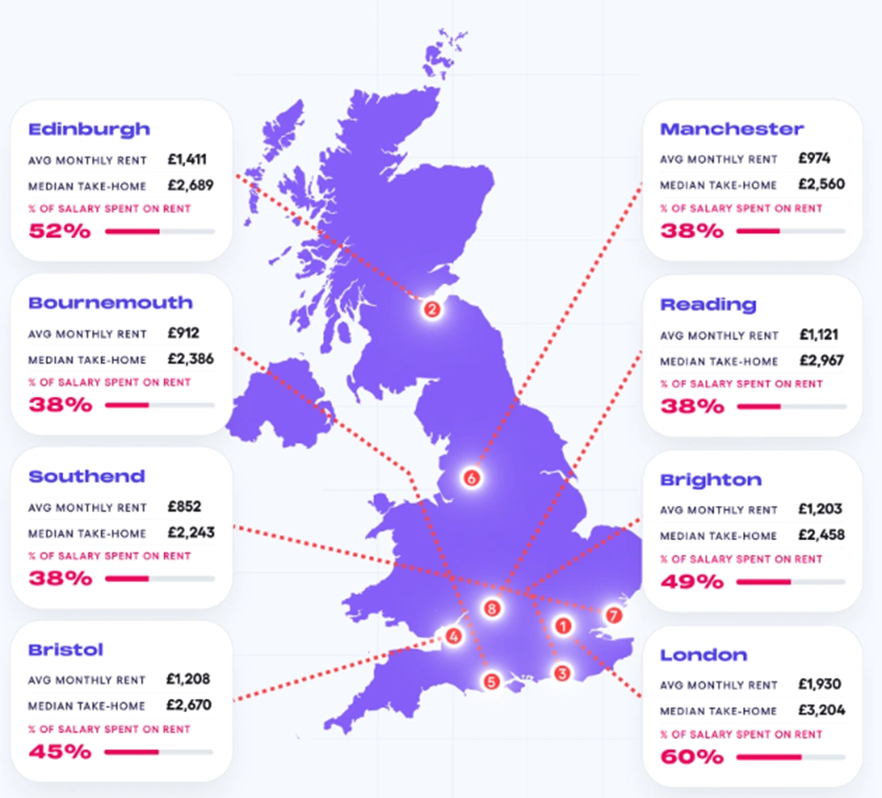

For those who do move out, the financial reality becomes clear quickly. The average private one‑bedroom rental is now about £1,107 per month, meaning someone earning the UK median salary of £39,000 would spend roughly 45% of their take‑home pay on rent alone.

However, national averages only tell part of the story. Rent levels and wages vary significantly across the country, making what is affordable in one area unreachable in another.

To assess the cost of living alone in the UK’s 30 largest towns and cities, we compared two factors: the average monthly rent for a one‑bedroom property and median monthly take‑home pay, assuming a 5% pension contribution (auto enrolment pension) and Plan 2 (or Plan 4 in Scotland) student loan repayments. We then calculated rent as a share of take‑home pay and the remaining disposable income.

London is the most expensive city in the UK for people living alone. A typical renter would spend around 60% of their take‑home pay on a one‑bedroom property, leaving approximately £1,274 per month from the city’s median salary of £54,340 before bills are included.

This represents the best‑case scenario. Someone earning closer to the UK median salary of £39,000 would need to allocate nearly 80% of their take‑home pay to rent, making independent living in London largely unaffordable.

Edinburgh ranks just behind London, with single renters spending around 52% of median take‑home pay on rent, while in Brighton the figure is just under 50%.

At the other end of the scale, Middlesbrough stands out as surprisingly affordable for solo renters. A median earner there would need to devote just 19% of their monthly take-home pay to rent – leaving over £2,000 to cover everything else.

The singles tax on everyday living

Rent is only one element of the overall cost of living. To understand how much more single people typically spend each month compared with couples who share expenses, we analysed the average essential bills for a single adult versus a couple living in a one‑bedroom home and maintaining a typical lifestyle, using data for costs that vary by household size such as food and transport.

Our analysis shows that single adults spend an additional £669.50 per month—more than £8,000 per year—compared with two people sharing the same household.

This includes:

• 50% higher council tax, even with the single‑person discount

• Around 50% higher water bills

• Approximately 30% higher communication costs, including phone and internet

• Over 10% higher food expenses

The only area where single people typically spend less is transport, at about 14% below the per‑person cost for couples. These higher expenses stem largely from the fact that many household costs do not scale down for one person. Fixed charges—such as standing energy fees, which amount to roughly £300 annually—apply regardless of occupancy. Smaller homes still require heating, and services like broadband and streaming subscriptions cost the same whether used by one person or several.

Food shopping also offers limited savings for single households because many products are sold in multi‑portion formats, often leading to higher per‑unit prices or increased waste. Taken together, these factors explain why living alone is considerably more expensive than intuition might suggest

Why Taxes Affect Solo Earners More Significantly

The financial impact of being single begins before you even spend any money. In the UK, tax is assessed on individual income rather than total household income. As a result, single earners often pay more tax than couples with an equivalent combined income, as couples can benefit from two personal allowances and keep more of their income within lower tax bands.

In other words, single earners often need to earn significantly more just to reach the same post-tax position as a working couple – and that’s before you even factor in higher bills and housing costs.

Single parents face even greater challenges.

Single parents face even greater financial pressures. Supporting a family on a single income leaves far less room for financial flexibility, and two in five single parents live in poverty.

Support is also withdrawn just as single parents begin earning a higher salary. Child Benefit starts to taper once income exceeds £60,000 and is removed entirely at £80,000. As a result, a single parent earning £80,000 with two children is around £2,000 worse off each year than two parents earning £40,000 each, despite the same combined income.

This imbalance extends to childcare support. Tax‑free childcare of up to £2,000 per child and 30 hours of funded childcare are only available if income stays below £100,000. A single parent earning £100,001 loses eligibility entirely, while a two‑parent household with a combined income of £200,000 can still receive full support.

Not all countries take the same approach to taxation. In France, income tax is assessed at the household level: total income is combined and then divided into a set number of “shares” based on the number of adults and children. Each additional child increases the number of shares, reducing the taxable income per share and limiting exposure to higher tax rates.

Luxembourg achieves a similar effect by offering single parents a more favourable tax classification than single adults without children, supplemented by a dedicated single‑parent tax credit.

The taxation on single individuals living in retirement

Single people do not receive much financial relief in retirement. The higher costs associated with living alone continue beyond working life. Pensions UK provides benchmarks for the income required to achieve different retirement living standards—from minimum to comfortable—depending on whether someone is single or part of a couple.

A single person must save substantially more than each member of a couple to achieve the same standard of living in retirement. This equates to 24% more for a minimum standard, 44% more for a moderate standard and 45% more for a comfortable standard.

Based on assumptions including full State Pension entitlement and a 2% real annual return over a 30‑year retirement, the required pension pots for single individuals are significantly higher than those for each partner in a couple.

The differences required to achieve the same retirement standard are substantial. It is not only a financial gap but also a time burden. With a £250 monthly pension contribution and a 5% annual growth rate, a single person would need to save for approximately 12 additional years compared with someone in a couple to reach a moderate retirement level.

Last thing to note as a single person

There is a common misconception that inheritance tax is paid by those receiving an inheritance. In reality, it is levied on the estate of the person who has died, provided their assets exceed the relevant thresholds. Who ultimately receives the money is considered only after the tax due has been settled.

The UK inheritance tax system generally benefits couples more than single individuals. Assets passed to a spouse or civil partner are typically exempt from inheritance tax, and any unused allowance from the first partner can be transferred to the survivor. As a result, a couple can combine two £325,000 nil‑rate bands and, where applicable, two £175,000 residence nil‑rate bands, allowing up to £1 million to be passed on tax‑free. In 2022–23, £5.98 billion was transferred to surviving spouses and civil partners under these rules.

Single people do not receive equivalent advantages. With no spouse exemption and no ability to transfer unused allowances, they have only one set of thresholds. Any assets above those limits are taxed at 40%, meaning their estates may reach the tax threshold more quickly and a larger proportion can be taken in tax.

Overall, the inheritance tax system—like many aspects of UK taxation—assumes and financially favours couplehood. While independence has many personal benefits, single individuals often face higher costs and fewer allowances, both during life and after death.

Getting sound financial planning advice is key.